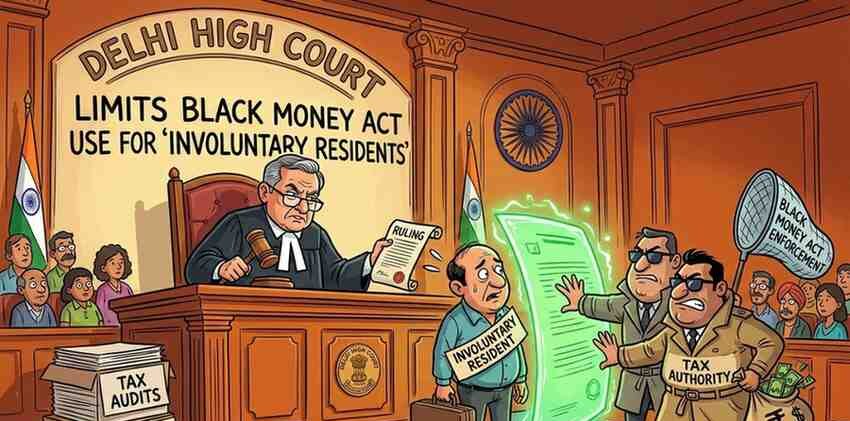

The Delhi High Court rules that the Black Money (Undisclosed Foreign Income and Assets) Act cannot be invoked against “involuntary residents” to compel foreign asset disclosure. Read a detailed 1000-word legal analysis, implications, and FAQs.

Introduction

In a significant ruling, the Delhi High Court has clarified the limits of the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (commonly known as the Black Money Act). The Court held that tax authorities cannot invoke this stringent law against individuals classified as “involuntary residents” — persons who became residents of India due to circumstances beyond their control, such as detention, travel restrictions, or inability to leave the country.

This judgment narrows the interpretational scope of the Act and strengthens safeguards against coercive tax enforcement where residency status arises involuntarily.

Background: Understanding the Black Money Act, 2015

The Black Money Act was enacted in 2015 to combat the problem of undisclosed foreign income and assets held by Indian residents abroad. It empowers authorities to:

- Tax undisclosed foreign income and assets at a flat rate of 30%.

- Impose severe penalties up to 90% of the undisclosed value.

- Initiate prosecution leading to imprisonment.

- Require detailed disclosure of overseas financial holdings.

The law applies primarily to residents of India under income tax rules. Therefore, residency status becomes a critical factor in determining liability under the Act.

What Is an “Involuntary Resident”?

Under Indian tax law, an individual qualifies as a “resident” if they satisfy certain stay criteria (typically 182 days or more in a financial year). However, in some cases, a person may remain in India longer than intended due to:

- Detention by authorities

- Passport impoundment

- Medical emergencies

- Travel bans

- Global disruptions (such as pandemics)

In such cases, their residency is not a result of voluntary presence but compulsion. These individuals are often referred to in legal arguments as “involuntary residents.”

Core Issue Before the Delhi High Court

The dispute arose when tax authorities attempted to invoke provisions of the Black Money Act against an individual who had become a tax resident during a period when they were allegedly unable to leave India due to compelling circumstances.

The authorities argued that once residency criteria are satisfied, the Act automatically applies — regardless of how that residency arose.

The petitioner challenged this interpretation, arguing that:

- The Act’s objective is to penalize deliberate concealment of foreign assets.

- Applying it to someone who unintentionally became a resident would be unjust.

- Coercive disclosure requirements cannot be imposed mechanically.

Delhi High Court’s Key Observations

The Delhi High Court took a purposive approach to statutory interpretation. Its major findings include:

Purpose of the Act Must Guide Interpretation

The Court emphasized that the Black Money Act was designed to target willful tax evasion and undisclosed foreign wealth, not individuals trapped by circumstances beyond their control.

Residency Must Be Meaningful, Not Merely Technical

While tax law defines residency based on days of stay, the Court recognized that mechanical application without contextual evaluation could lead to injustice.

Protection Against Arbitrary Enforcement

The judgment reinforces constitutional safeguards under Article 14 (Right to Equality) by preventing arbitrary or disproportionate use of penal tax provisions.

Coercive Disclosure Powers Cannot Be Misused

Authorities cannot use the Act merely as a tool to compel disclosure where the foundational condition — legitimate resident status tied to intentional presence — is questionable.

Legal Significance of the Judgment

This ruling is important for several reasons:

Clarifies Scope of Black Money Act

It prevents blanket application of the Act in cases where residency is involuntary.

Strengthens Due Process

The judgment reinforces that penal tax statutes must be interpreted strictly and reasonably.

Limits Executive Overreach

Tax authorities must assess factual circumstances before initiating proceedings under stringent laws.

Provides Relief to Non-Resident Indians (NRIs)

NRIs who were stranded in India due to extraordinary events may now have stronger legal grounds to contest similar notices.

Constitutional Dimensions

The decision reflects broader constitutional principles:

- Article 14 (Equality Before Law) – Prevents arbitrary application of harsh penalties.

- Article 21 (Right to Life and Personal Liberty) – Protects individuals from excessive state action impacting liberty through criminal prosecution.

- Doctrine of proportionality – Ensures penalties correspond to the nature of wrongdoing.

By interpreting the statute in line with these principles, the Court reaffirmed judicial oversight over executive taxation powers.

Implications for Tax Authorities

The ruling may lead to:

- More cautious issuance of notices under the Black Money Act.

- Greater scrutiny before labeling individuals as residents for foreign asset reporting.

- Potential revision of internal guidelines for enforcement.

Authorities will now likely need to consider:

- Whether residency arose voluntarily.

- Whether the individual had genuine control over their stay in India.

- The intent behind non-disclosure, if any.

Impact on Taxpayers and NRIs

This judgment provides clarity and reassurance to:

- Business professionals stranded in India.

- Foreign citizens temporarily stuck due to emergencies.

- Individuals facing passport or legal restrictions.

However, it does not dilute the Act for genuine tax evaders. The Black Money Act continues to apply strictly to individuals who intentionally conceal foreign income or assets while being legitimate residents.

Broader Policy Implications

The decision may influence:

- Future legislative amendments clarifying residency in extraordinary circumstances.

- Litigation strategy in tax enforcement disputes.

- Judicial approach in interpreting other penal economic laws.

It signals that while combating black money remains a priority, enforcement must remain fair, proportionate, and constitutionally sound.

Conclusion

The Delhi High Court’s ruling marks an important development in Indian tax jurisprudence. By restricting the application of the Black Money Act against “involuntary residents,” the Court has reinforced the principle that harsh penal statutes must not be applied mechanically.

The judgment balances two competing interests: the State’s legitimate goal of combating black money and the individual’s right to fair treatment under the law. In doing so, it strengthens constitutional protections while preserving the integrity of India’s tax enforcement framework.

As tax regulations grow increasingly stringent in a globalized financial environment, judicial oversight remains essential to ensure fairness, proportionality, and accountability in enforcement.

Frequently Asked Questions: Delhi High Court Limits Black Money Act

What did the Delhi High Court rule in this case?

The Delhi High Court ruled that the Black Money Act cannot be invoked against individuals who became residents of India involuntarily, such as due to detention or inability to travel abroad.

What is the Black Money (Undisclosed Foreign Income and Assets) Act, 2015?

It is a stringent Indian law aimed at taxing and penalizing undisclosed foreign income and assets held by Indian residents. It includes heavy penalties and possible imprisonment.

Who qualifies as an “involuntary resident”?

An involuntary resident is someone who becomes a tax resident due to circumstances beyond their control, such as travel restrictions, detention, medical emergencies, or global crises.

What should someone do if they receive a notice under the Black Money Act?

They should immediately consult a qualified tax lawyer or chartered accountant to evaluate whether residency status and disclosure obligations are validly invoked.